Disruption or Opportunity? Reframing Financial SaaS in the Age of AI

Where Is the Value Now? Rethinking Financial SaaS After the AI Shock

Markets are forward-looking — but not always accurate.

The sell-off in financial SaaS reflects a growing belief that AI will compress margins, erode data moats, and commoditise insight. But current pricing suggests something more extreme: a rapid and structural decline in business models that, historically, have proven highly resilient.

The question is not whether AI will impact the sector — but whether the magnitude and timing of that impact are being misjudged.

The release of Anthropic’s latest Claude model in mid-February has accelerated these concerns. Positioned as a highly capable reasoning engine with strong performance in financial analysis, document interpretation, and code generation, Claude signals a shift from static data access toward dynamic, AI-generated insight. Tasks that traditionally required expensive terminals or structured datasets — from summarising earnings reports to building basic financial models — can now be executed in seconds through natural language interfaces.

This technological leap is forcing investors to reassess the durability of traditional financial SaaS value propositions. If AI can replicate parts of the analytical workflow at a fraction of the cost, the perceived moat around data platforms begins to narrow. However, what the market may be overlooking is that these platforms are not merely data providers — they are deeply embedded in institutional workflows, compliance frameworks, and decision-making processes. The real question is not whether AI can generate insight, but whether it can replace the trust, accuracy, and integration that enterprise clients require at scale.

To assess whether this repricing reflects structural risk or emerging opportunity, it is necessary to move beyond the narrative and examine the data at the company level. Despite a shared exposure to AI-driven disruption, financial SaaS firms are not equally positioned — differences in valuation, analyst sentiment, capital allocation, and near-term catalysts suggest a more nuanced picture. The following analysis breaks down key players individually to identify where the market may be overreacting, and where underlying fundamentals continue to support long-term value.

🟡 Morningstar (MORN) — Recovery Play

Morningstar is best known for its star rating system and analyst ratings, including the widely recognized Gold, Silver, and Bronze fund ratings. It is also a leading investment research firm, primarily through its flagship Direct platform.

The company owns several prominent businesses, including PitchBook, one of the leading private equity data and research platforms; Sustainalytics, a major provider of ESG research and ratings; and DBRS Morningstar, the fourth-largest credit rating agency globally.

In recent years, Morningstar has increasingly invested in benchmark and index services to strengthen its position in this market.

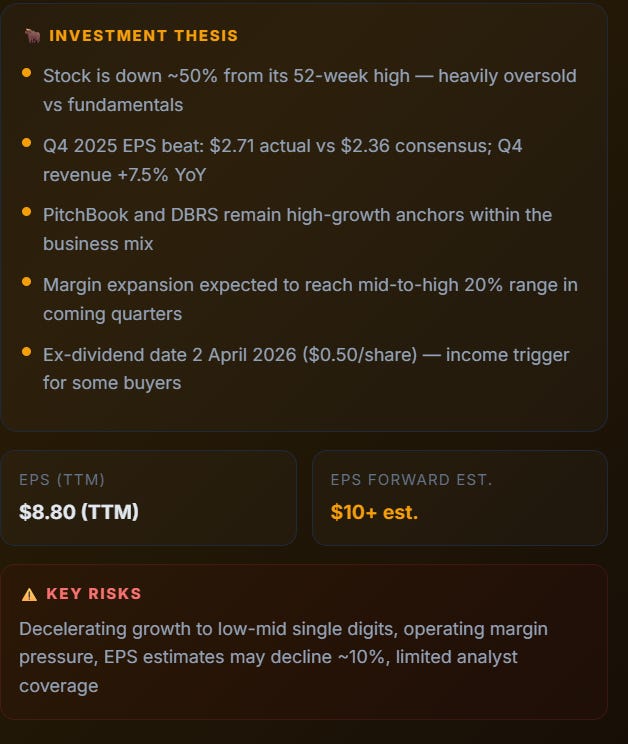

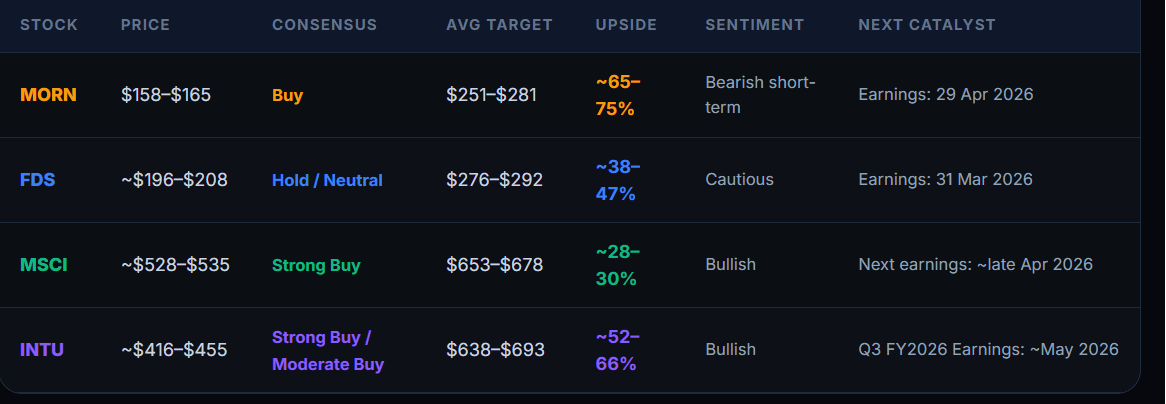

MORN stock is sitting near its 52-week low of $156.81, down roughly 56% from its high of $358. Only 3 analysts cover it, but all are bullish with an average target of $251–$281 — implying ~65–75% upside. A sell signal was issued from a pivot top on 9 March 2026 and the stock has since fallen ~14%; technicals remain weak short-term.

However, despite a Buy consensus among Wall Street analysts, some bearish signals are emerging. BMO Capital Markets recently lowered its price target to $193, while UBS maintained its Buy rating with a $280 target.

In addition, the company is facing pressure on operating margins, with earnings per share potentially declining by around 10%.

🔵 FactSet (FDS) — Value Opportunity

FactSet is a global financial data and analytics provider, offering integrated solutions to investment professionals across asset management, investment banking, and wealth management. Its platform combines proprietary datasets, third-party content, and advanced analytics tools into a single workflow, enabling users to perform research, portfolio analysis, and financial modeling efficiently.

The company operates on a subscription-based model, characterised by high recurring revenue and strong client retention. Over time, FactSet has expanded its capabilities through strategic acquisitions and product development, particularly in areas such as data integration, ESG analytics, and workflow automation, positioning itself as a key infrastructure provider within the financial services ecosystem.

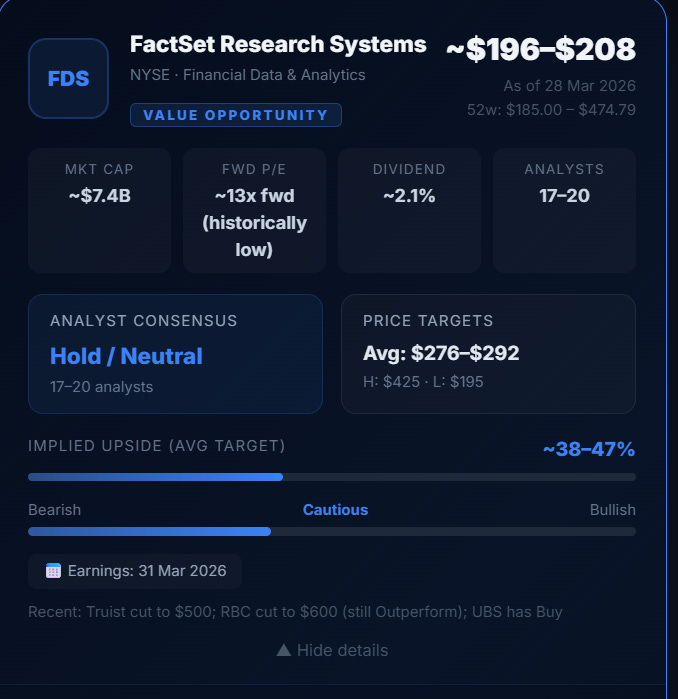

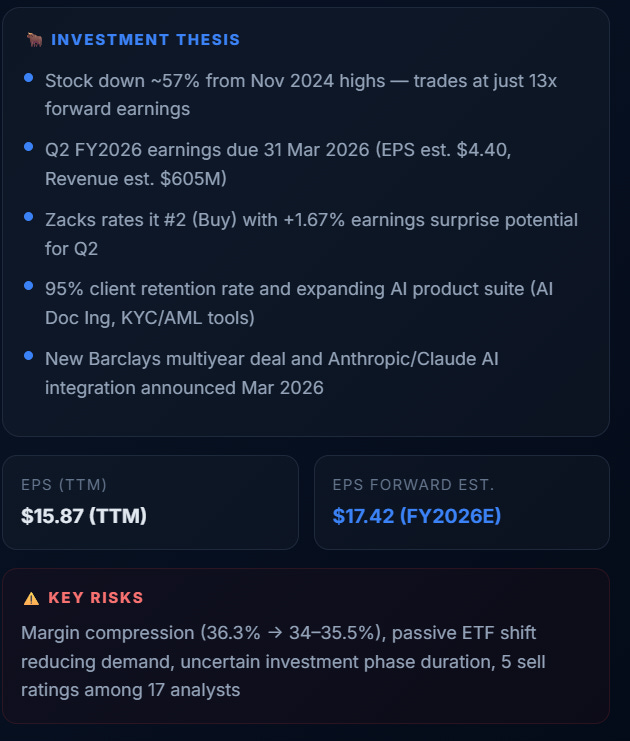

FDS is around $198, down nearly 60% from its November 2024 high. FDS stock’s mean price target of $289.88 implies ~47% upside potential, with the street-high at $425 suggesting 115% from current levels. Critically, the stock’s year-to-date decline of ~32% versus a 4.2% decline for the benchmark signals persistent selling pressure and fragile sentiment. Q2 FY2026 earnings are due 31 March 2026 — a major near-term catalyst, with analysts forecasting EPS of $4.40 and revenue of $605M.

On the positive side, the company has recently secured strategic partnerships with Barclays and Anthropic, the developer of Claude, which could support future growth and innovation.

The key risks relate to potential margin compression, with operating margins expected to decline from 36.3% to a range of 34%–35.5%. Additional concerns include weakening demand for passive ETFs and uncertainty around the duration of the current investment cycle.

It is also worth noting that 5 out of 17 analysts maintain Sell ratings, indicating a degree of skepticism despite the broader consensus.

🟢 MSCI (MSCI) — Strongest Conviction

MSCI is a leading provider of investment decision support tools, best known for its global equity indices, including the widely tracked MSCI World and MSCI Emerging Markets benchmarks. The company serves asset managers, asset owners, and financial institutions with a broad suite of solutions spanning index construction, portfolio analytics, risk management, and ESG research.

Its business model is highly scalable and largely subscription-based, with a significant portion of revenue linked to assets under management (AUM) tied to MSCI indices. This creates strong operating leverage and recurring revenue streams, positioning MSCI as a core infrastructure provider in global capital markets. Over time, the firm has expanded into ESG and climate analytics, further strengthening its role in long-term investment decision-making.

As of 27–28 March 2026, MSCI is trading around $528–$535 with an average 12-month price target of $678, and 15 analysts recommending buy versus just 1 sell — implying ~28% upside. Raymond James upgraded MSCI to Strong Buy with a $710 target in March 2026. On the positive side, is also that zero sell ratings from the major houses makes this the most broadly bullish name in the group.

However, MSCI continues to trade at a relatively high price-to-earnings (P/E) multiple. Growth in asset-backed finance (ABF) is also moderating, declining from 20.8% to around 15%.

In addition, recent insider selling by the CFO may raise concerns among investors.

🟣 Intuit (INTU) — High-Conviction Tech

Intuit is a leading financial software company focused on providing solutions for individuals, small businesses, and accountants. Its core products, including TurboTax, QuickBooks, and Credit Karma, support tax preparation, accounting, and personal finance management, forming a highly integrated ecosystem.

The company operates a subscription-driven and services-based model with strong recurring revenue and high customer retention. In recent years, Intuit has increasingly incorporated AI and automation into its platforms to enhance user experience, streamline financial workflows, and expand its addressable market, positioning itself at the intersection of fintech and intelligent financial services.

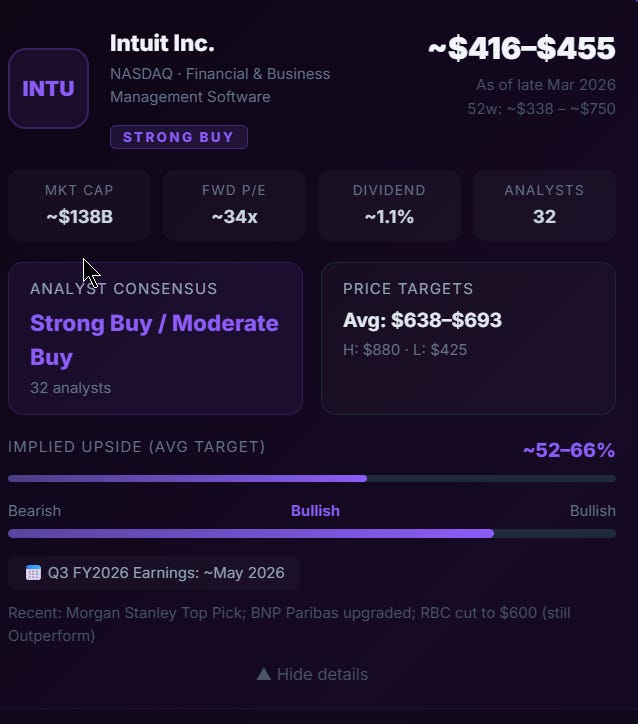

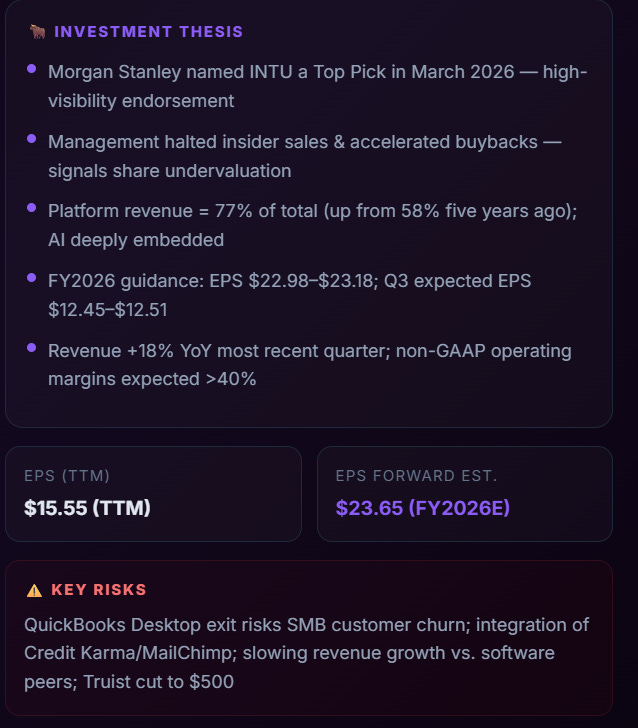

21 analysts have a Buy consensus as of March 2026 with an average price target of ~$693 Public, implying ~52–66% upside from the current ~$416–$455 range. Morgan Stanley named Intuit a Top Pick in March 2026; management halted planned insider stock sales and accelerated buybacks — a signal that leadership believes the stock is undervalued.

The key risks relate to potential churn among small and medium-sized businesses (SMBs) using QuickBooks Desktop, as well as challenges associated with integrating Credit Karma and Mailchimp into the broader ecosystem. Intuit also faces relatively slower revenue growth compared to its software peers.

In addition, Truist Securities recently lowered its price target for Intuit to $500.

Conclusion

The recent sell-off across Morningstar, FactSet, MSCI, and Intuit reflects a market increasingly focused on the potential disruptive impact of AI.

However, the data suggests a more nuanced reality. Despite short-term bearish sentiment and technical weakness — particularly in Morningstar and FactSet — analyst consensus remains broadly positive, with upside potential ranging from approximately 28% to 75% across the group. This divergence indicates that while the market is pricing in near-term uncertainty, it may be overestimating the speed and severity of structural disruption.

At the same time, upcoming earnings releases across all four companies represent key catalysts that could either validate current concerns or trigger a re-rating.

In this context, the sector appears to be transitioning from a narrative-driven sell-off to a fundamentals-driven reassessment.

💡 Investment Perspective (Not financial advice — analytical view)

🟢 1. MSCI — Highest Quality / Lowest Risk

Strong Buy consensus

Most stable sentiment

Consistent business model (index + AUM-linked revenues)

👉 Best for:

✔ Conservative investors

✔ Long-term compounding

✔ Lower volatility exposure

🟣 2. Intuit — Growth + Conviction Play

Strong Buy across analysts

High upside (~50–65%)

Management confidence (buybacks, insider signals)

👉 Best for:

✔ Growth investors

✔ AI + fintech exposure

✔ Medium-term upside

🔵 3. Morningstar — Deep Value / Turnaround

~50% drawdown

High implied upside (~65–75%)

Weak short-term sentiment

👉 Best for:

✔ Contrarian investors

✔ Value seekers

✔ Willingness to accept short-term volatility

🔵 4. FactSet — Mixed / Watchlist

Neutral sentiment

Persistent selling pressure

Upcoming earnings critical

👉 Best for:

✔ Monitoring, not aggressive entry

✔ Post-earnings positioning

Subscribe to Dividends Journey for expert insights on dividend investing: Subscribe Here.

Need personalised guidance, talk about your investment or want to start from scratch and build a portfolio? Book a 1-on-1 consultation with me today: Schedule a Call.

Start making smarter investment decisions now! 🚀📈

Disclaimer: This content is for informational purposes only and does not constitute financial advice. We are not licensed financial advisors. Please consult a professional before making investment decisions.